A White Paper on Regulatory Risk and Strategic Readiness for Digital Platforms Operating in India

Version 1.0 | June 2026

Executive Summary

India is preparing one of the world’s most consequential digital market regulations: the Digital Competition Bill (DCB). Modeled on the European Union’s Digital Markets Act but adapted to India’s domestic context, the DCB proposes an ex-ante regulatory framework that would impose proactive compliance obligations on a small set of “Systemically Significant Digital Enterprises” (SSDEs) — large platforms in search, app stores, ad tech, operating systems, cloud, browsers, and e-commerce.

Unlike the existing Competition Act of 2002, which acts only after anti-competitive harm has occurred, the DCB would require designated firms to comply with conduct rules from day one — restrictions on self-preferencing, data combination across services, anti-steering provisions, and mandatory interoperability. As of mid-2026, the Bill remains in pre-legislative consultation, with the Ministry of Corporate Affairs reviewing over 100 stakeholder submissions and signaling no rushed timeline.

For global technology companies with significant Indian user bases — search and app store operators, social platforms, e-commerce marketplaces, and cloud providers — the strategic question is not whether such regulation arrives, but when and in what form. This paper outlines the Bill’s likely structure, draws lessons from the EU’s DMA enforcement experience, and recommends a readiness framework for affected enterprises.

Section 1: Why India Is Building Its Own Digital Markets Act

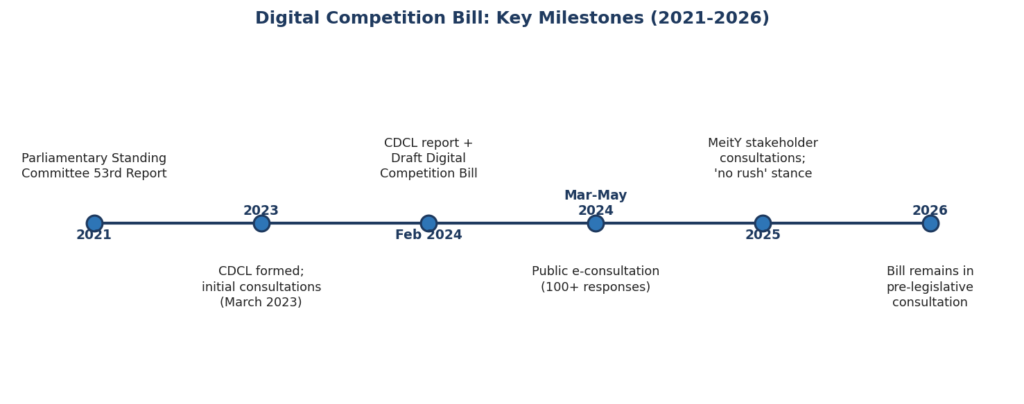

India’s digital economy has scaled rapidly, and with it, concerns about concentrated market power. The Parliamentary Standing Committee on Finance’s 53rd report on “Anti-Competitive Practices by Big Tech Companies” concluded that the existing Competition Act’s case-by-case, after-the-fact enforcement model is structurally too slow for digital markets, where dominant positions can become entrenched — or “tip” irreversibly — within months.The ex-post framework under the Competition Act of 2002 fails to promptly address anti-competitive conduct, and the present framework may not be effective in addressing the irreversible tipping of markets in favour of large digital enterprises.

In response, the Ministry of Corporate Affairs formed the Committee on Digital Competition Law (CDCL), a 16-member expert body that spent roughly a year studying global frameworks before producing a report and draft Bill.The proposed law is inspired by the European regulatory model and is designed to prevent anti-competitive practices, ensure transparency, and curb unfair favouritism in the digital sector.

KEY STAT: India’s digital economy is projected to reach $800 billion by 2030 — a scale that regulators argue justifies proactive market-structure rules rather than waiting for harm to materialize.

Section 2: How the Bill Defines “Big Tech” — The SSDE Threshold

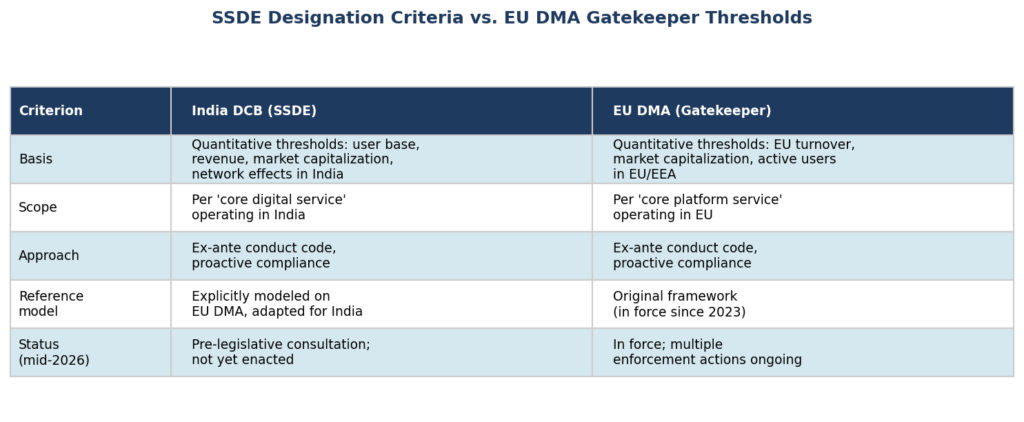

The DCB’s central regulatory mechanism is the designation of Systemically Significant Digital Enterprises (SSDEs).The Bill establishes the concept of SSDEs — platforms meeting specific quantitative thresholds related to user base, revenue generation, market capitalization, and network effects within Indian operations.

This is a deliberate echo of the DMA’s “gatekeeper” concept.SSDEs are enterprises that provide core digital services in India and have a significant presence and significant financial strength in the country, modeled on the EU’s Digital Markets Act, which regulates large online platforms known as gatekeepers to prevent anti-competitive practices and promote a more open and competitive digital market.

In practice, this means a relatively small number of global platforms — likely including major search engines, app store operators, social networks, operating system providers, browsers, cloud infrastructure providers, and large e-commerce marketplaces — would face a separate compliance regime layered on top of existing competition law.

Once designated, an SSDE would not wait for a regulator to prove harm. Instead, it would need to demonstrate ongoing compliance with a defined code of conduct across every “core digital service” it operates in India.

Section 3: The Conduct Code — What Changes for Designated Platforms

While the final text remains under consultation, the direction signaled by the CDCL report and comparable global frameworks points to a consistent set of obligations for SSDEs:

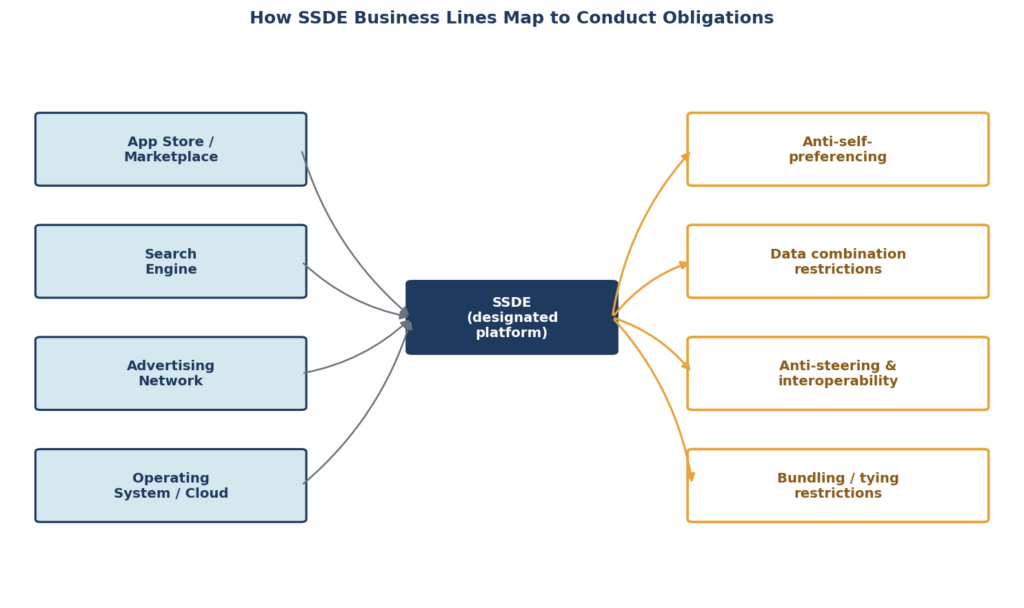

Anti-self-preferencing. Platforms that both operate a marketplace and compete within it (e.g., an app store that also sells its own apps, or an e-commerce platform with house brands) would face restrictions on ranking their own products or services above competitors’.

Data use restrictions. SSDEs would face limits on combining user data collected from one service to benefit another service within the same corporate group — a direct response to concerns that conglomerate-scale platforms can leverage data advantages across unrelated product lines.

Anti-steering and interoperability. Business users (app developers, sellers, advertisers) would gain stronger rights to direct customers to alternative payment or communication channels outside the platform, and in some cases, rights to interoperate with platform infrastructure.

Bundling and tying restrictions. Pre-installation of an SSDE’s own apps as a condition of using its operating system, or bundling of services as a non-removable default, would come under scrutiny — directly echoing concerns already litigated in India’s Android-related antitrust cases.

KEY STAT: Over 100 stakeholder responses were submitted during the Ministry of Corporate Affairs’ public e-consultation on the draft Bill, reflecting unusually high engagement from technology companies, industry associations, and legal think tanks.

Section 4: Where the Bill Faces Pushback — and Why That Matters for Timing

The consultation process has surfaced substantive concerns that affect how — and how soon — the Bill might move forward.

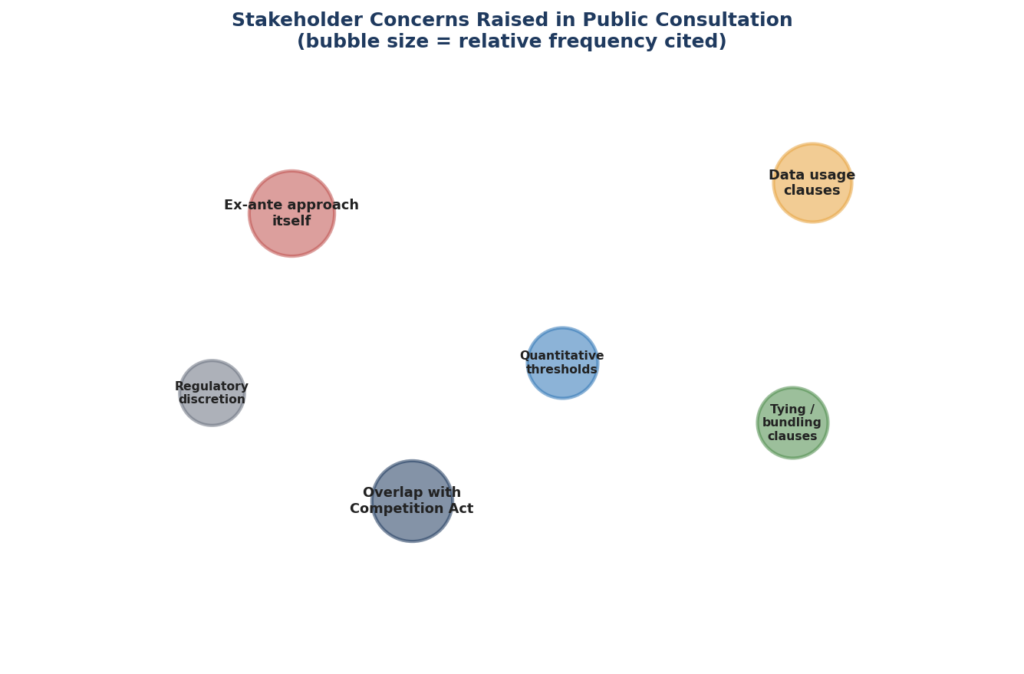

Reconsidering ex-ante regulation itself. Stakeholders questioned the need to reconsider the ex-ante regulatory approach, the use of quantitative thresholds, and specific clauses related to data usage and tying or bundling of services. This is not a minor drafting note — it goes to the core architecture of the law.

Regulatory overlap and forum-shopping risk. Industry analysts have flagged that the Bill might overlap with provisions in the current Competition Act, leading to regulatory complexity, potential confusion, and the possibility of parallel inquiries with divergent rulings for the same conduct under different laws.

Discretionary power concerns. A recurring theme in commentary is that the ex-ante approach may give regulators excessive discretionary power, raising concerns about potential misuse — a worry amplified by India’s relatively young experience with proactive digital regulation compared to the EU’s decades of competition enforcement infrastructure.

On timing, the government has been explicit that it is not rushing. The Indian government is not in a hurry to bring the Digital Competition Bill and wants to follow due process with further deliberations on the proposed legislation before introducing it. The Minister of State for Corporate Affairs has emphasized that the Digital Competition Bill will follow a comprehensive legislative process before being finalized, with the central government intending to thoroughly review proposed revisions before proceeding with implementation.

Section 5: Lessons from the EU’s Digital Markets Act Experience

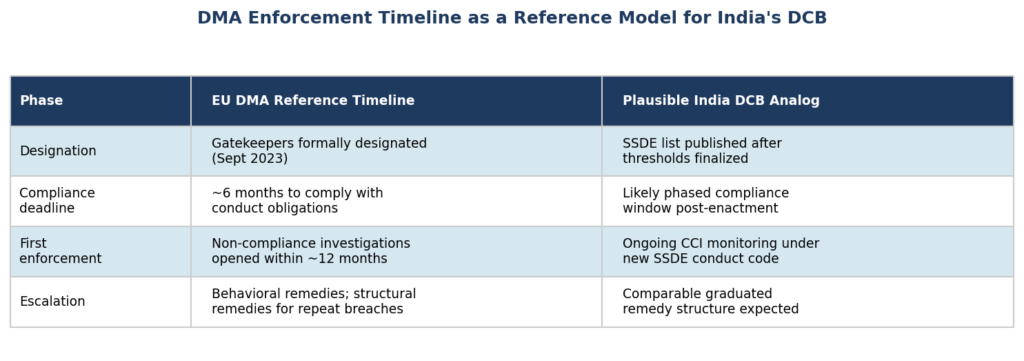

Because the DCB is explicitly modeled on the DMA, India’s regulators and affected companies alike have a live testbed to draw from. Three lessons stand out:

1. Designation is the real battleground. Much of the DMA’s early enforcement energy went into disputes over which services qualify as “core platform services” and which corporate entities count as gatekeepers. Companies operating in India should expect similar definitional contests — and should not assume that only the most obvious global giants will be designated; mid-tier platforms with strong network effects in specific Indian verticals (e-commerce, ride-hailing, food delivery, fintech super-apps) could plausibly meet SSDE thresholds even without global gatekeeper status.

2. Compliance is operational, not just legal. DMA compliance required gatekeepers to re-architect product flows — default settings, consent screens, app store policies, and data-sharing pipelines — not merely update terms of service. The DCB’s anticipated provisions on data combination and self-preferencing would likely demand comparable engineering and product changes, not just legal memos.

3. Enforcement cadence shapes commercial risk. The EU model shows that designated firms face a continuous compliance relationship with regulators — periodic reporting, audits, and the possibility of behavioral remedies escalating to structural ones for repeat non-compliance. Indian firms preparing for the DCB should plan for an ongoing regulatory relationship, not a one-time legal review.

KEY STAT: The DCB draws on regulatory reference points from the EU, UK, Australia, and Japan — jurisdictions where ex-ante digital market rules are at varying stages of implementation and litigation.

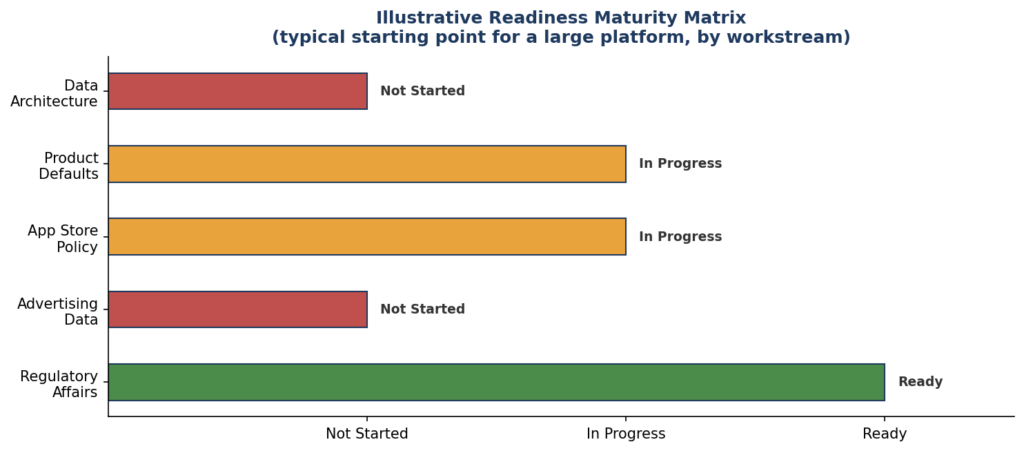

Section 6: Readiness Framework for Affected Platforms

Given the consultative pace of the Bill, companies have a window — but not an indefinite one — to prepare. A practical readiness approach includes:

Map exposure by business line, not by corporate entity. Because SSDE designation is likely to apply per “core digital service,” a single company may have some India business lines in scope (e.g., an app store) and others out of scope (e.g., a niche enterprise tool), even within the same legal entity.

Audit data flows between services now. Restrictions on cross-service data combination are among the most operationally disruptive provisions in comparable laws. Understanding which data currently flows between an India search product, an ad network, and an app marketplace — and why — is foundational diligence that takes months, not weeks.

Track the consultation process directly. The Ministry of Corporate Affairs has followed its Pre-Legislative Consultation Policy closely, including multiple public comment rounds.Consultations on the Draft Digital Competition Bill were conducted in consonance with the Pre-Legislative Consultation Policy of the Ministry of Corporate Affairs, gathering responses from a diverse group of stakeholders following the committee’s report and draft bill in February 2024. Future consultation windows are the clearest early signal of the Bill’s evolving scope and timeline.

Build a cross-functional compliance task force early. The DMA experience suggests that legal, product, engineering, and policy teams need a shared compliance roadmap well before designation occurs — retrofitting compliance after designation is materially more costly and disruptive than designing for it in advance.

[DATA VIZ: Readiness checklist / maturity matrix — five workstreams (data architecture, product defaults, app store policy, advertising data, regulatory affairs) scored against three readiness stages]

Conclusion and Recommendations

Three takeaways define the current moment for technology platforms operating in India:

- The direction of travel is clear, even if the timeline is not. India has committed to an ex-ante digital competition framework modeled on the EU’s DMA; the open questions are about scope, thresholds, and sequencing — not whether such a law will eventually exist.

- Designation criteria will determine exposure more than brand recognition. Quantitative thresholds tied to Indian user base, revenue, and network effects mean that companies should assess exposure on a service-by-service basis rather than assuming only the largest global names are at risk.

- The compliance burden is operational, not just legal. Based on comparable frameworks, the most resource-intensive work — re-architecting data flows, default settings, and platform policies — takes far longer than the legislative process itself, making early preparation a genuine competitive advantage.

Recommendation: Affected companies should commission an SSDE-exposure assessment now, focused on mapping India-facing business lines against the emerging designation criteria and auditing inter-service data flows — the two areas most likely to require lead time regardless of the Bill’s final form.

Data Visualization Plan

- Section 1 — Timeline: Parliamentary Standing Committee report → CDCL formation → draft Bill → consultation rounds

- Section 2 — Comparison table: SSDE designation criteria vs. EU DMA gatekeeper thresholds

- Section 3 — Flow diagram: SSDE business units mapped to applicable conduct obligations

- Section 4 — Bubble chart: stakeholder concerns by frequency across consultation responses

- Section 5 — Comparison table: DMA enforcement timeline as a reference model

- Section 6 — Readiness maturity matrix across five compliance workstreams

References

- Ministry of Corporate Affairs, Government of India. Rajya Sabha Unstarred Question No. 2944, answered August 19, 2025 — Status of the Draft Digital Competition Bill. Via TaxGuru.

- “Digital Competition Bill,” PMF IAS, current affairs briefing, May 2026.

- “Digital Competition Bill 2026: SSDE Rules for E-commerce Platforms in India,” Startup Solicitors LLP, February 2026.

- “India’s Digital Competition Bill Advances with Industry Insights,” India Briefing, March 2025.

- “Govt to bring Digital Competition Bill after due process: Harsh Malhotra,” Business Standard, March 16, 2025.

- “Understanding the Draft Digital Competition Bill: Key Proposals and Implications,” Vajiram & Ravi, October 2025.