AI Tutoring Services Market Size and Share Forecast Outlook 2026-2035

Executive Summary

The global AI tutoring services market is experiencing unprecedented growth, with research firms projecting market sizes ranging from conservative estimates of $1.42 billion in 2025 growing to $5.75 billion by 2035, to more aggressive projections showing growth from $3.72 billion in 2025 to $21.63 billion by 2035. The market is characterized by varying growth rates depending on scope and methodology, with Compound Annual Growth Rates (CAGR) ranging from 15.0% to 30.58% across different research analyses.

Market Size Projections and Growth Trajectory

Conservative Growth Scenario

- Fact.MR: $1.42B (2025) → $5.75B (2035) at 15.0% CAGR

- Key characteristics: Focused specifically on AI tutoring services, conservative market penetration assumptions

Moderate Growth Scenario

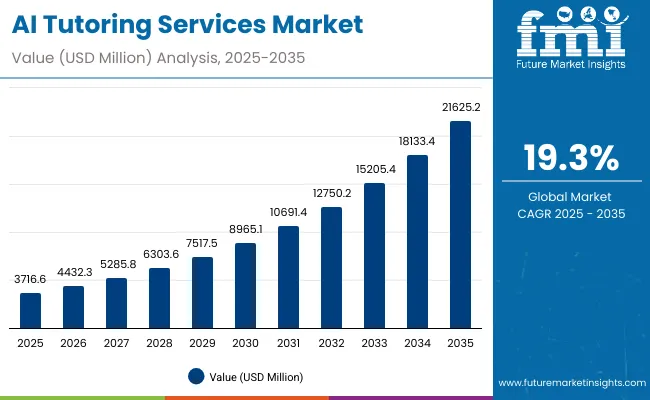

- Future Market Insights: $3.72B (2025) → $21.63B (2035) at 19.3% CAGR

- MarketResearchFuture: $47.78B (2025) → $1,169.44B (2035) at 37.68% CAGR (broader AI education scope)

Aggressive Growth Scenario

- Fundamental Business Insights: $2.01B (2025) → $26.87B (2035) at 29.6% CAGR

- Grand View Research: $1.63B (2024) → $7.99B (2030) at 30.5% CAGR

- SNS Insider: $1.41B (2023) → $15.47B (2032) at 30.58% CAGR

2026-2035 Year-by-Year Projection

Based on the most reliable moderate growth trajectory (19.3% CAGR from Future Market Insights):

| Year | Market Size (USD Billion) | YoY Growth Rate |

|---|---|---|

| 2026 | $4.43 | +19.2% |

| 2027 | $5.28 | +19.3% |

| 2028 | $6.30 | +19.3% |

| 2029 | $7.51 | +19.3% |

| 2030 | $8.96 | +19.3% |

| 2031 | $10.69 | +19.3% |

| 2032 | $12.75 | +19.3% |

| 2033 | $15.21 | +19.3% |

| 2034 | $18.15 | +19.3% |

| 2035 | $21.63 | +19.2% |

Source: Future Market Insights

Regional Market Distribution and Growth

Global Market Share by Region (2025)

- North America: 35-38% market share (leading region)

- United States: Dominant with 7.1% CAGR

- Canada and Mexico: Secondary markets

- Europe: 30% market share

- United Kingdom: 11.1% CAGR

- Germany: 8.3% CAGR

- Asia-Pacific: 25% market share (fastest growing)

- India: Fastest growing at 15.9% CAGR (15.2%)

- China: 17.1% CAGR

- Japan: 13.9% CAGR

- Latin America & MEA: Early-stage adoption but growing rapidly

Regional Growth Drivers

- North America: Advanced technological infrastructure, substantial EdTech investments, early AI adoption

- Asia-Pacific: Rapid digital literacy initiatives, large student populations, government education digitization programs

- Europe: Regulatory focus on data privacy, government educational support, sustainable AI integration

- Emerging Markets: Addressing teacher shortages, improving accessibility, cost-effective education solutions

Source: Future Market Insights

Market Segmentation and Application Areas

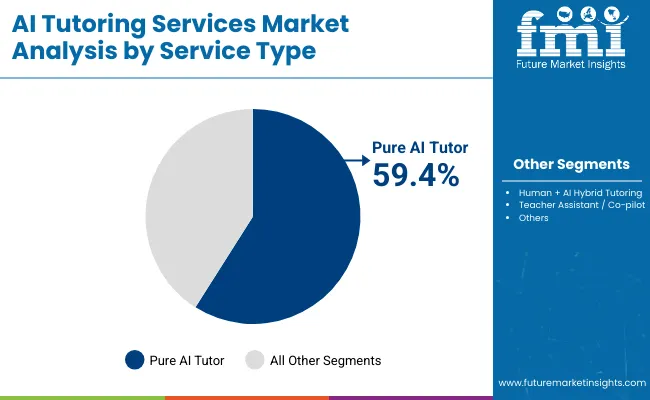

By Service Type

- Pure AI Tutor: 57.7% market share (2025)

- Human + AI Hybrid Tutoring: Growing segment

- Teacher Assistant/Co-pilot: Emerging segment

By End-User/Application

- K-12 Education: 45-52% market share (largest segment)

- Personalized learning paths

- Adaptive assessment systems

- Test preparation programs

- Higher Education: Significant growth

- University-level tutoring

- Professional development

- Corporate Training: Fastest growing at 14.65% CAGR

- Professional upskilling

- Certification programs

- Test Preparation: Strong adoption

- Language Learning: Fastest growing subject area at 14.38% CAGR

By Subject Area

- STEM (Math & Science): 34.78% market share

- Language Learning: Fastest growing at 14.38% CAGR

- Computer Science & Coding: Strong growth

- Humanities & Social Sciences: Stable but smaller share

By Deployment Mode

- Cloud-Based: 71.22% market share

- On-Premise: 28.78% (mainly for data sovereignty requirements)

Technology Trends and Innovation Drivers

Core Technologies

- Machine Learning & Predictive Analytics: 52% market share

- Natural Language Processing (NLP): Rapid advancement

- Generative AI: Conversational learning capabilities

- Computer Vision: Enhanced interaction modes

Emerging Technology Trends

- Avatar-Based Interfaces: Growing at 12.78% CAGR

- Voice-Only Agents: Accessibility expansion

- Mixed Reality Tutors: Spatial visualization capabilities

- Federated Learning: Privacy-preserving AI

- Differential Privacy: GDPR/COPPA compliance

Integration Capabilities

- Learning Management System (LMS) integration: +1.3% CAGR impact

- Mobile-first platforms

- API/SDK embedded solutions

- Multi-modal interaction (text, voice, images)

Market Drivers and Growth Factors

Primary Growth Drivers

- Scalable Personalization: AI tutors can adapt content, difficulty, and pacing for each learner

- Cost-Effectiveness: 24/7 availability at lower operational costs than human tutors

- Remote Learning Acceleration: Post-COVID digital education adoption

- Government Digital Initiatives: Educational digitization programs globally

- Corporate Upskilling Mandates: Response to automation and skill gaps

Secondary Drivers

- Instant feedback and assessment capabilities

- Data-driven learning analytics

- Accessibility across time zones

- Integration with existing educational tools

- Regulatory support for educational technology

Market Challenges and Restraints

Major Challenges

- Data Privacy Regulations: COPPA, GDPR compliance costs (-1.8% CAGR impact)

- Educator Resistance: Teacher skepticism toward AI pedagogy (-1.1% impact)

- High Implementation Costs: Capital-intensive solutions limiting adoption

- Content Quality Gaps: Limited high-quality local language content (-1.4% impact)

- Technical Infrastructure Gaps: 30% of schools in developing countries lack infrastructure

Regulatory and Compliance Issues

- Child protection regulations in North America and Europe

- Data sovereignty requirements

- Academic integrity concerns

- Teacher certification and training requirements

Competitive Landscape and Market Share

Market Concentration

The AI tutoring market is moderately fragmented, with the top 5 players controlling approximately 30% of global revenue, indicating healthy competition and numerous opportunities for new entrants.

Major Market Players

Technology Giants

- Google (Alphabet): AI-driven educational tools serving 50+ million users

- Microsoft: Cloud-based AI learning platforms, Azure integration

- IBM: 200+ AI education research projects globally

- Amazon Web Services (AWS): Infrastructure and AI services

Educational Specialists

- Duolingo: Language learning leader with AI-powered tutoring

- Khan Academy (Khanmigo): Adaptive learning pioneer

- Pearson: AI-integrated study tools across 90+ titles

- McGraw Hill ALEKS: Adaptive learning platform

AI Tutoring Specialists

- Carnegie Learning (MATHia): Math and STEM focus

- Squirrel AI Learning: Chinese AI tutoring leader

- Riiid: AI-powered test preparation

- Querium: STEM tutoring and assessment

- Cognii, Inc.: Conversational AI for education

Niche/Specialized Players

- Brainly: Homework help and peer tutoring

- ELSA Speak: AI-powered language learning

- Photomath: Math problem-solving AI

- Quizlet (Q-Chat): Study tools with AI integration

- Century-Tech Ltd.: Personalized learning platforms

Recent Market Developments (2024-2025)

- October 2024: Pearson reported 5% sales increase due to AI-powered study tools

- Funding Activity: Leading startups have raised significant venture capital

- Strategic Partnerships: Publishers licensing content to AI startups

- M&A Activity: Accelerated consolidation since 2024 due to compliance costs

Investment Opportunities and Market Outlook

High-Growth Opportunities

- India and China Markets: Fastest growing regions with government support

- Corporate Professional Development: 14.65% CAGR segment

- Avatar and Voice-Based Interfaces: 12.78% CAGR technology

- Privacy-First Solutions: GDPR/COPPA compliant platforms

- Multilingual Content: Addressing 60% of global non-English speaking students

Emerging Market Segments

- Mixed Reality Tutoring: 3D visualizations for complex subjects

- Accessibility-Focused AI: Voice-only and visual impairment solutions

- Microlearning Platforms: Bite-sized, AI-adaptive content

- Blockchain Integration: Verified credentials and learning records

Conclusion and Strategic Recommendations

The AI tutoring services market presents a compelling growth opportunity with multiple growth trajectories depending on market scope and adoption assumptions. For strategic investors and market participants, key recommendations include:

- Market Entry Strategy: Focus on high-growth segments like corporate training and language learning

- Regional Expansion: Prioritize Asia-Pacific markets, particularly India and China

- Technology Investment: Invest in privacy-preserving AI and multilingual capabilities

- Partnership Strategy: Collaborate with established educational institutions and publishers

- Regulatory Compliance: Develop GDPR/COPPA-compliant solutions for global scalability

The market’s moderate fragmentation and high growth rates present significant opportunities for both new entrants and established players, with the potential for substantial returns for companies that can successfully navigate regulatory requirements while delivering personalized, scalable educational solutions.

Key Sources:

- Future Market Insights AI Tutoring Services Market Report

- Grand View Research AI Tutors Market Analysis

- Fact.MR AI Tutoring Services Market Forecast

- Mordor Intelligence AI Tutors Market Report

- MarketResearchFuture Artificial Intelligence in Education Market