There are more than a thousand individual IRS tax forms — enough for anyone to get lost in — but fortunately, the vast majority of these forms are irrelevant for the everyday U.S. tax filer.

But which forms do you need to be aware of?

We’ve rounded up some of the most important and commonly used tax forms so you can see which ones are relevant to you and the important details you need to know about them.

First, let’s quickly consider a shortlist of which forms are likely relevant to you based on your employment status and source of income to save you some time.

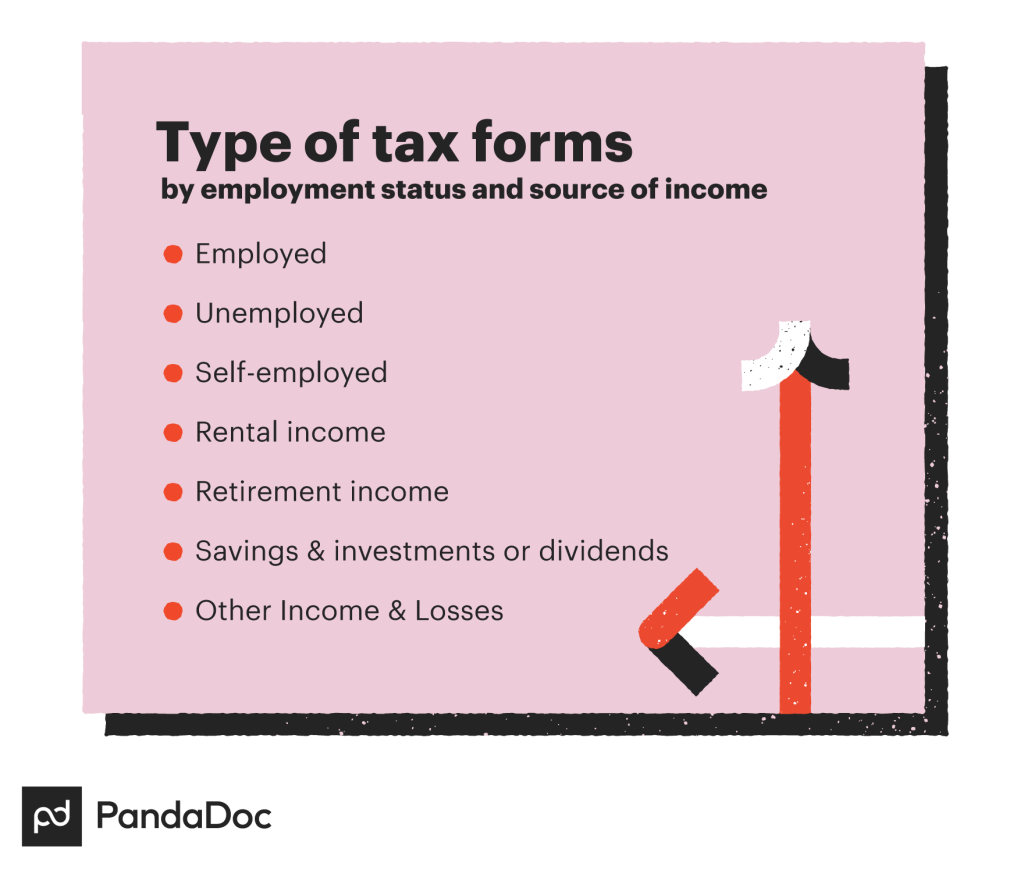

List of forms by employment status and source of income

You’ll need to use different tax forms based on the source of your income and your employment status. Not all of the listed forms necessarily need to be filed every year.

Many of them depend on whether you had any applicable activity that requires that type of filing, such as distributions, capital gains or losses, gambling income, etc.

The main tax forms that most U.S. tax filers should concern themselves with are available in PandaDoc’s accounting and tax templates.

Here’s a quick checklist of important forms and documents you’ll need to be aware of based on your employment status and income sources, with more detail on the specific IRS forms to follow afterward.

Employed

- Form W-2

- State Tax Withholding form

Unemployed

Self-employed

- Form 1099, Schedules K-1, 1099-NEC, or income records to verify amounts not reported on 1099-MISC

- Record of approximate tax payments made (Form 1040–ES)

- Records of expenses — credit card statements, check registers, and receipts

- Business-use asset information (date place in service, cost, etc.) for depreciation

- In-home office information, if applicable

Retirement income

- Pension/IRA/annuity income (1099-R)

- Social security/RRB income (SSA-1099, RRB-1099)

- Traditional IRA basis (i.e., all your nondeductible contributions and nontaxable amounts included in rollovers made to IRAs after subtracting the total of all your nontaxable distributions)

Rental income

- Records of income and expenses

- Rental asset information (initiation date, cost, etc.) for calculating depreciation

- Record of approximate tax payments made (Form 1040–ES)

Other income and losses

- Gambling income (W-2G or records showing income along with expense records)

- Hobby income and expenses

- Jury duty records

- State tax refund

- Awards and prizes

- Trust income

- Royalty Income (1099–MISC)

- Record of alimony paid or received including ex-spouse’s name and SSN

- Any other 1099s received

Savings and investments or dividends

- Interest, dividend income (1099-INT,1099-DIV, 1099-OID)

- Income from sales of stock or property (1099-B, 1099-S)

- Purchases or sales of cryptocurrency

- Dates of acquisition and records of your costs in any property you sold (if not already reported on 1099-B)

- Expenses related to your investments

- Health Savings Account and long-term care reimbursements (1099-LTC or 1099-SA)

- Record of approximate tax payments made (Form 1040–ES)

Overview of IRS tax forms

Now that you have a better idea of which tax forms likely apply to you, we’ll dive into the basics of the most important and common IRS forms so that you know what they do, who needs to file them, and any other relevant details. Staying informed about any updates or revisions to tax codes is crucial for accurate and compliant filing. Tax laws and regulations can change from year to year, so subscribing to reliable tax news sources or consulting with a tax professional who can provide guidance on the latest changes is essential. This proactive approach ensures that you’re well-prepared to navigate the evolving landscape of tax requirements, including understanding how Arizona sales tax may affect your financial situation. Depending on your business activities and presence in the state, you may have obligations to collect and remit sales tax. Familiarising yourself with the specific requirements and rates applicable in Arizona can prevent costly oversights or errors when filing your returns. It’s advisable to keep meticulous records of all sales transactions within the state, as this will not only streamline the filing process but also serve as a safeguard in case of any future audits or inquiries. By staying informed about Arizona sales tax regulations, you’ll be better equipped to fulfil your tax obligations effectively and in compliance with state laws. Remember, staying updated on tax regulations is a key step towards maximising your deductions and minimising potential liabilities come tax season.

It’s also worth pointing out that a number of the tax forms we’ll be discussing are available in PandaDoc’s database of templates and can make for a more straightforward, streamlined filing process.

01. Form 1040, U.S. individual income tax return

If you’re a working U.S. citizen that makes an income of over $12,500, you’ll need to complete a Form 1040, which is the individual Income Tax Return document.

The IRS uses this form to calculate your personal income taxes, but it’s also an extremely important form for declaring your filing status, claiming potential credits, taking standard deductions, and ultimately, figuring out how much money you owe the IRS.

This is the baseline form that most Americans will need to complete come tax season.

02. Form 1040-EZ, US income tax return for single and joint filers with no dependents

If you have a relatively uncomplicated tax situation with no joint filers and no dependents, you might be able to take a more streamlined approach by filing the short-version tax form, Form 1040-EZ.

Besides being a single filer with no dependents, you’ll also need to be under 65 years old with a taxable income that’s less than $100,000 to qualify.

There are some other requirements such as having a taxable interest of $1,500 or less, no household employment taxes on wages paid to a household employee owing, etc.

You’ll want to review the full list of requirements before submitting this form.

03. Form 1040-SR, US tax return for seniors

Taxpaying seniors over the age of 65 have Form 1040-SR available to them as an alternative to the standard Form 1040.

This form is designed to be easier for seniors to read, with fewer complications and a more straightforward method of documenting common sources of income, such as IRA distributions, Social Security, investment income, and annuities.

04. Form 1040X, amended U.S. individual income tax return

No one wants to make a mistake on their Form 1040 when it’s submitted, but unfortunately, it happens to many tax filers every year. If you find yourself in a situation where you need to amend your Form 1040, you’ll use a Form 1040X.

Though it’s predominantly used for correcting previously filed tax returns, it can also be used to change amounts previously adjusted by the IRS, claim carrybacks due to unused credit or losses, and make certain tax elections after the deadline.

05. Schedule A to Form 1040, itemized deductions

As a taxpayer, you can take advantage of standard deductions or itemized deductions. Standard deductions are prescribed amounts that can be subtracted from a person’s taxable income.

They don’t require an item-by-item analysis on the individual’s part, whereas itemized deductions are more exhaustive and thorough.

If you have itemized deductions that total more than the standard deduction you would receive, then it might make sense to use a Schedule A form to itemize your deductions. Schedule A is attached to Form 1040 when you submit your tax return.

06. Schedule C to Form 1040, profit or loss from business (sole proprietorship)

If you’re a self-employed individual, you might need to file a Schedule C with your tax return to report how much money was made or lost in your business.

The various categories of applicable expenses include meals and entertainment, travel, insurance, taxes, wages, office supplies, and other business-related items.

07. Schedule D to Form 1040, capital gains and losses

Investors who trade bonds, stocks, or other instruments will likely be required to submit a Schedule D in addition to Form 1040. Schedule D forms allow you to tally your capital gains and losses for the year (e.g., stocks you sold for a profit or for a loss).

Up to $3,000 of your net losses could be deductible, but you can carry excess losses forward to the following year using another Schedule D.

Capital losses that exceed the current year’s gains may be carried forward as well using Schedule D.

08. Schedules K-1 to Form 1041, beneficiary’s share of income, deductions, credits, etc.

If you’ve invested in a limited partnership (LP) or exchange-traded fund (ETF), you’ll likely be issued a Schedule K-1. The data on this document is used to report your share of earnings, losses, credits, and deductions on your Form 1040.

09. Form W-2, wage and tax statement

W-2 forms are issued by employers every year, and it’s a very important document that you’ll want to make sure you hold onto since it documents how much an employee was paid in a year.

This W-2 form (or an IRS-approved substitute) acts as a record of retirement plan contributions, the value of workplace benefits, and how much state and federal income taxes were withheld.

It’s a critical document for determining how much you paid in taxes over the course of a year, and you should be issued one by your employer by January 31 each year.

10. Form W-4, employee’s withholding certificate

The W-4 form is used to figure out how much federal income tax should be withheld from your paycheck by your employer.

New employees should receive a W-4 to complete, and employees should file a W-4 with their employer each year or when their personal or financial situation changes in a significant way, like having a baby or getting married.

There are only five steps involved in completing a W-4 form, so the process is fairly straightforward.

11. Form W-4P, withholding certificate for pension or annuity payments

If you have a pension or receive an annuity (i.e., an agreement with an insurance provider that pays you a fixed sum of money each year), a Form W-4P will be used to navigate the rules in place for these payments and to determine how much federal income tax will need to be withheld.

This form is applicable for U.S. citizens and their estates as well as for resident aliens.

12. Form 1099-MISC, miscellaneous income

As the name implies, Form 1099-MISC is used to report miscellaneous income of anything more than $600 in a full tax year. It can be used to report income from royalties, rents, prizes, awards, and other sources.

It was previously used to report non-employee compensation for independent contractors, freelancers, sole proprietors, and self-employed individuals, but as of the 2020 tax year, that’s no longer the case as non-employee income is now reported on a separate form called the 1099-NEC.

13. Form 1099-G, certain government payments

The 1099-G form is used by taxpayers to report any government payments that have been received, such as unemployment compensation or state or local income tax refunds.

It’s also used for reporting taxable grants and any payments received from the Department of Agriculture. All of these payments are taxable and must be included on your year-end tax return.

14. Form 1099-K, payment card and third party network transactions

In 2011, Form 1099-K was created for taxpayers who received payments through a third-party network or who accepted merchant cards for payments.

Payments from third-party networks such as Uber or Lyft have grown over the years, making this a more relevant form for thousands of taxpayers.

In the past, taxpayers were required to complete this form after gross earnings exceeded $20,000 and the number of transactions exceeded 200 in a calendar year.

For example, an Uber driver who performs 200 rides and is paid over $20,000 would need to submit this form. As of 2021, however, the threshold for reporting was lowered from $20,000 to $600, meaning many more taxpayers will need to use this form.

15. Form 1099-R, distributions from pensions, annuities, IRAs retirement plans, insurance contracts, etc.

If you’re retired and receiving payments or distributions of some kind, you’ll likely receive a 1099-R form since it deals specifically with passive income and retirement plans.

Specifically, anyone who receives a distribution of $10 or more from an IRA, a profit-sharing or retirement plan, an annuity, a pension, a survivor income benefit plan, an insurance contract, a disability payment under a life insurance contract, or a charitable gift annuity, should receive a 1099-R from the plan issuer.

16. Form 1099-S, proceeds from real estate transactions

If you’ve been part of an exchange of real estate or received certain royalty payments in the tax year, you should receive a 1099-S to report the proceeds.

Transactions could include land, permanent structures, condominium units, or stock in a cooperative housing corporation, to name a few.

17. 1099-INT, interest income

If you earned more than $10 in interest for the calendar year, you should receive Form 1099-INT from your brokerage, bank, or other financial institution.

This form is used to report various kinds of interest like tax-exempt interest, interest income from brokerages and banks, and interest on U.S. Savings Bonds and Treasury obligations.

Every amount listed on the form needs to be added to your return, and if the total taxable interest is over the $1,500 threshold, you must prepare and attach a Schedule B with the name of the payer and the amount received.

18. Form 1099-DIV, dividends and distributions

Many companies pay dividends to their shareholders, and those dividends need to be reported to the IRS.

If your money is handled by an investment manager, they should supply you with Form 1099-DIV or an IRS-approved substitute that notes any dividends and capital gains distributions received in the calendar year.

This form will also disclose your ordinary versus qualified dividends (i.e., payments which may qualify for taxation at lower rates).

19. SSA-1099, social security benefit statement

If you’ve received Social Security benefits in the tax year, you’ll be issued an SSA-1099 (also called a 1042S Benefit Statement or SSA-1042S) in the January following so that you know how much of the income to report to the IRS on your tax return.

These forms are not used for people who receive Supplemental Security Income (SSI) or for non-citizens who live outside of the United States. Non-citizens will receive an SSA-1042S instead.

20. Form 8917, tuition and fees deduction

Students or anyone responsible for paying college tuition expenses can use an 8917 form to determine how much has been paid in tuition and fees to an eligible postsecondary educational institution in the tax year.

The expenses paid may qualify you for certain tax credits or deductions.

21. Form 1098, mortgage interest statement

If you paid a minimum of $600 in mortgage interest in the calendar year, you’re eligible to claim a deduction and should ideally receive this form as a reminder of how much you paid.

Single filers and married couples filing jointly can deduct interest on up to $750,000.

Ultimately, each individual taxpayer is responsible to keep track of their mortgage interest payments, because lenders aren’t required to send one.

Considering standard deductions go as high as $18,650 for households, it’s well worth the effort.

22. Form 1095-A, health insurance marketplace statement

Anyone receiving health insurance from the marketplace will receive Form 1095-A online in their HealthCare.gov account or in the mail.

You’ll need this form before filing your tax returns because it includes the premiums you’ve paid in the year and any applicable premium tax credits.

Final points taxpayers should be aware of

There’s no shortage of IRS tax forms, but you will most likely need to make use of one or just a few. Whichever forms you need to file, make sure to always confirm that you’re using the correct version for the current tax year.

Also, be mindful of situational changes in your life that may require you to submit fewer or more forms going forward.

Remember that each tax year is tied to the calendar year, meaning a new tax year starts on January 1 of each year. Form issuance and payment dates vary on a case-by-case basis, so if you’re expecting a certain form, double-check the date you should receive it to make sure it comes.

The same goes for payments you may owe, as you’ll want to make sure you make the payments by the due date to avoid interest charges.

For an even easier tax filing process, you also might want to check out PandaDoc’s database of accounting and tax templates.

Finally, when in doubt, consult an accountant or appropriate tax filing professional for assistance with your personal situation.

Looking For Document Management System?

Call Pursho @ 0731-6725516

Check PURSHO WRYTES Automatic Content Generator

https://wrytes.purshology.com/home

Telegram Group One Must Follow :

For Startups: https://t.me/daily_business_reads