(NY shown as ~21 calendar days to approximate 15 business days; TX shows the outside 45-day window when extra time is noticed. Always rely on your own state’s exact wording.) Texas StatutesLegal Information Institute

Real-world example

After a winter pipe break, a homeowner received a low repair estimate that ignored code upgrades. They responded with a short letter citing their Ordinance or Law coverage, enclosed the contractor’s itemized bid and building-department correction notice, and referenced the state’s decision deadline. The carrier re-inspected, added code items, and increased payment by 38%.

Use the version that fits your situation. Replace bracketed items and attach the evidence listed.

1) Coverage denial you believe is wrong (causation dispute)

Subject: Request for reconsideration of denial — [Policy No.], Claim [#], Date of Loss [MM/DD/YYYY]

[Your Name]

[Address] • [Phone] • [Email]

[Date]

[Claims Department / Adjuster Name]

[Insurer Name]

[Insurer Address]

Dear [Adjuster Name],

I am writing to dispute the denial of my homeowners claim dated [denial date] regarding water damage discovered on [loss date]. Your letter cites “wear and tear” and “repeated leakage” as grounds for denial. The facts and enclosed documentation show a sudden, accidental discharge due to a burst supply line during freezing temperatures, which is a covered peril under Section I – Perils Insured Against of my HO policy.

Evidence enclosed

-

Licensed plumber report confirming a sudden line burst on [date]

-

Photos and time-stamped video from the discovery date

-

Weather records for [city] showing freeze conditions on [dates]

-

Dry-out logs and moisture readings within 24 hours of discovery

Policy and law

-

Section I – Perils Insured Against covers sudden and accidental discharge from plumbing.

-

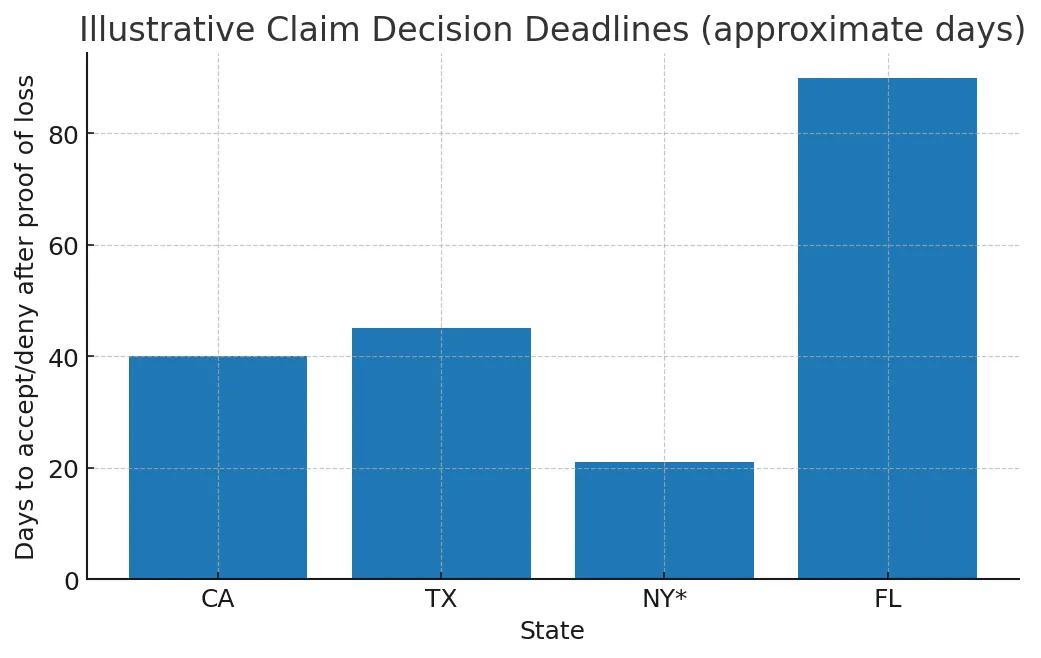

If more information is needed, please specify in writing. In California, for example, an insurer must accept or deny a claim within 40 days of receiving proof of claim and provide written updates if more time is necessary. Similar prompt-payment standards apply in other states. Legal Information Institute

Requested action

Please reverse the denial or identify precisely what additional documentation you require. If coverage is accepted, kindly issue payment for undisputed amounts within the required timeframe. In New York, once there is an agreement, payment must be issued within five business days. Legal Information Institute

I appreciate written confirmation within 14 days of receipt of this letter. I am available for re-inspection upon request.

Sincerely,

[Your Name]

Attachments: plumber report; photos; weather records; mitigation invoices.

2) Payout is too low (scope/price dispute — ask for reinspection or appraisal)

Subject: Undervaluation dispute and demand for reinspection/appraisal — [Policy No.], Claim [#]

Dear [Adjuster Name],

Thank you for your estimate dated [date]. It omits matching of materials and code upgrades required by our local building department. My independent estimate (enclosed) details proper scope, quantities, and pricing, including [e.g., ICC/Ordinance or Law] coverage.

Please schedule a reinspection within 10 business days. If we cannot agree on the amount of loss, I hereby make a written demand for appraisal per the policy appraisal clause. As standard HO-3 language provides: “If you and we fail to agree on the amount of loss, either may demand an appraisal… Each party will choose a competent and impartial appraiser within 20 days…” III

Evidence enclosed

-

Licensed contractor/Xactimate estimate with line items

-

Building department notice requiring code upgrades

-

Product sheets showing discontinued materials for matching

Please confirm your availability for reinspection or provide your appraiser’s contact within 7 days.

Sincerely,

[Your Name]

Attachments: estimate; code notice; product documentation.

3) Delay without clear updates (nudge with timelines)

Subject: Status request and compliance with claim time standards — [Policy No.], Claim [#]

Dear [Adjuster Name],

I appreciate your work on my claim. It has been [X] days since I submitted the completed proof of loss and supporting documents on [date]. Please advise in writing whether the claim is accepted or denied and what amounts are undisputed.

Regulators expect timely decisions. As an example, California requires a written accept/deny decision within 40 days of proof of claim and written status updates every 30 days if more time is needed. Texas requires timely acknowledgments and allows up to 45 days to decide after notifying the claimant that more time is needed. Legal Information InstituteTexas Statutes

Kindly provide a status update and any additional information needed within 10 calendar days.

Sincerely,

[Your Name]

Attachments: proof-of-loss; submission receipt; correspondence log.

4) Roof claim denied for “late notice” (show diligence and prejudice)

Subject: Reconsideration of denial for alleged late reporting — [Policy No.], Claim [#]

Dear [Adjuster Name],

Your denial dated [date] cites “late notice.” I reported the claim promptly after discovering interior staining on [date]. Before that date, no interior leaks were visible and the roof surface looked intact from ground level. I acted with reasonable diligence once the damage could be discovered.

Please re-evaluate the decision. I enclose a roofer’s report, photos, and a repair invoice showing wind-lifted shingles consistent with the storm on [storm date]. Where applicable, please note that carriers are expected to conduct a thorough, fair, and objective investigation before denying a claim. hinshawlaw.com

If you maintain a late-notice defense, please explain how the timing prejudiced your investigation. Otherwise, please accept coverage and issue undisputed payment in the required timeframe.

Sincerely,

[Your Name]

Attachments: roofer report; weather data; photos; invoice.

5) Partial payment after catastrophe (use mediation/complaint for leverage)

Subject: Request for mediation / complaint notice — [Policy No.], Claim [#] (Hurricane/Disaster)

Dear [Adjuster Name],

Thank you for your payment dated [date]. It does not cover code upgrades, temporary housing extensions, or full replacement of [items]. I would like to resolve this efficiently.

I am requesting state-sponsored mediation to help us reach agreement (available in Florida for residential property claims). Please confirm your participation or provide a supervisor contact so we can schedule within 15 days. If needed, I will also file a department complaint to facilitate a timely, impartial review. FLDFSNAIC

Enclosed is updated documentation of my covered losses and living expenses. I remain available for reinspection.

Sincerely,

[Your Name]

Attachments: updated estimate; code notices; ALE receipts; photos.

Pro tips to improve results (field-tested)

-

Make it skimmable: Put your ask in the first paragraph and bold key numbers.

-

Stack credible proof: Independent estimates, dated photos, and building-department notices beat opinions.

-

Use compliant language: Quote your exact policy section and the relevant regulation (e.g., CA 10 CCR §2695.7(b); NY Reg. 64). Legal Information Institute+1

-

Set fair deadlines: 7–14 days for a reinspection or written response is reasonable.

-

Escalate smartly: Reinspection → Appraisal (amount-of-loss disputes) → Mediation/Complaint → Counsel if needed. IIIFLDFSNAIC

Short statistics & quotes you can reuse in your letters

-

“Customer satisfaction with homeowners insurance property claims declines to a seven-year low.” (J.D. Power, 2024) J.D. Power

-

“Insurer shall pay or deny [a residential property] claim within 90 days after notice.” (Florida §627.70131) The Florida Senate

-

“Insurer must accept or deny within 40 days of proof of claim.” (California §2695.7(b)) Legal Information Institute

-

“Pay any amount finally agreed upon within five business days.” (New York Reg. 64) Legal Information Institute

-

Lightning claims: $1.27B paid in 2023; average cost up 14.6% year-over-year. (Triple-I) III

Frequently used attachments checklist

-

Independent contractor or public adjuster estimate (itemized, room-by-room)

-

Photos/videos (before/after if available), moisture logs

-

City or county code notices; permits; inspector comments

-

Receipts for mitigation, temporary repairs, or ALE (Additional Living Expense)

-

Weather data (NOAA, local station), credit-card statements for emergency buys

-

Communication log (dates, who said what)

When to consider appraisal, mediation, or a complaint

-

Appraisal: Use when you agree there’s coverage but disagree on amount of loss. Policies typically let either party demand appraisal in writing, each selecting an impartial appraiser, with an umpire resolving differences. IIIiaua.us

-

Mediation: Some states offer pre-suit mediation for residential property claims (e.g., Florida DFS). It’s fast, informal, and often free to you. FLDFS

-

Complaint: If you hit a wall, file with your state insurance department; it can prompt overdue responses and course-corrections. NAIC

Mini-FAQ

How many follow-ups are too many?

Two polite written nudges a week apart are fine. Keep everything in writing.

What if the adjuster keeps changing?

Send your dispute letter to the general claims email too, and keep your claim diary current so hand-offs don’t erase progress. United Policyholders

Can I recover code upgrades?

Often yes, under Ordinance or Law coverage—check your Declarations and Loss Settlement provisions. Matthiesen, Wickert & Lehrer S.C.

Final word

Dispute letters work because they give your insurer a clear path to say “yes”: facts, policy, proof, and a reasonable deadline. In today’s claims environment, crowded, time-pressed, and audit-heavy, the most persuasive letter is the one that is easiest to pay.

This article is for general education; claim laws vary by state and policy. Consider local counsel for legal advice in your jurisdiction.

Looking For Document Management System?

Call Pursho @ 0731-6725516

Check PURSHO WRYTES Automatic Content Generator

https://wrytes.purshology.com/home

Telegram Group One Must Follow :

For Startups: https://t.me/daily_business_reads